You’ve saved up for decades, you’ve reached the day that you finally stop work, and the rest of your life stretches out before you. So why are you suddenly nervous about going out and spending your hard-earned cash?

On one hand, you might look at your pot and immediately book that round-the-world cruise. Or you might look at it and wonder how on Earth it’s going to last you for 20, 30, or even 40 years.

To avoid depleting their fund too quickly, many retirees make the mistake of being too cautious in retirement. Here’s why.

Keeping your money in cash often means it loses value in real terms

It’s easy to understand why you might want to take the fruits of your labour and ‘bank’ your pension pot at retirement. You might think about moving it all to somewhere where it’s guaranteed and won’t lose value. If you left it in the stock market, its value might fall, and you don’t want that risk.

However, think about it this way. If the return you’re getting on your savings isn’t keeping pace with inflation, it is losing value. Assuming an inflation rate of 2% (the Bank of England target), something that costs you £100 in 2020 will cost more than £148 in 20 years’ time. So, if you invest now, that £100 would have to grow to £148 in 20 years just to be worth the same in real terms.

In October 2020, the Consumer Prices Index (CPI) in the UK was 0.7%. So far, so good. Prices are not rising very fast, which means that your money will go further. However, recent research from Moneyfacts found that there were no easy-access savings accounts that paid an interest rate higher than inflation (unless you’re an existing customer of the ICICI Bank).

Simply put, if you invest your money in an easy-access savings account now, it’s highly unlikely to keep pace with inflation.

If you were prepared to tie your money up in a fixed-rate bond, then you have dozens more choices. But, with inflation set to rise in 2021, you may not be making a ‘real’ return for long.

So, what can you do about it?

Cash v shares – what’s the long-term comparison?

As you approach retirement, you might decide to move some of your fund into cash. As an investor, you might be worried that stock market volatility will affect your portfolio. You’ve worked hard to save that money and you don’t want to lose it!

Alternatively, you might decide to keep your fund invested – even as you start drawing down an income from it. Over time, stock market returns will a) generally exceed returns from cash and b) typically outstrip the inflation rate even though there may well be sharp corrections in markets.

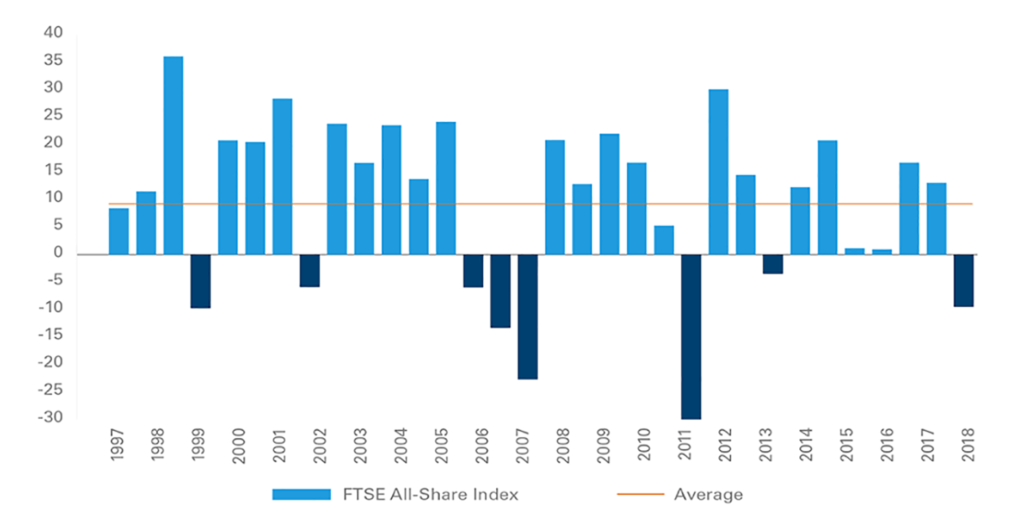

For example, here are the calendar-year returns for the FTSE All-Share Index over the past 30 years.

Source: Vanguard

The chart shows that there have been eight years during this period where returns were negative. However, the average annual return over the whole period is 9.9% – even taking the dotcom bubble and the global financial crisis into account.

It’s not just UK equities that have generated a good return over time. The MSCI World Index – an index covering 23 developed market countries including the UK, US, Germany, and Japan – shows that global markets have also produced positive returns.

Here’s the annualised returns of the MSCI World Index over one, three, five and ten years, and since its launch at the end of 1987.

Source: MSCI

Over the last decade, the index shows an annualised return of 10.81%. Between 31 December 1987 and 30 November 2020, the annualised return of global equities was 8.21%.

Shares vs other asset classes

Over time, equities in the UK and the wider world tend to generate positive returns, despite some short-term turmoil.

But how do equities compare to other asset classes?

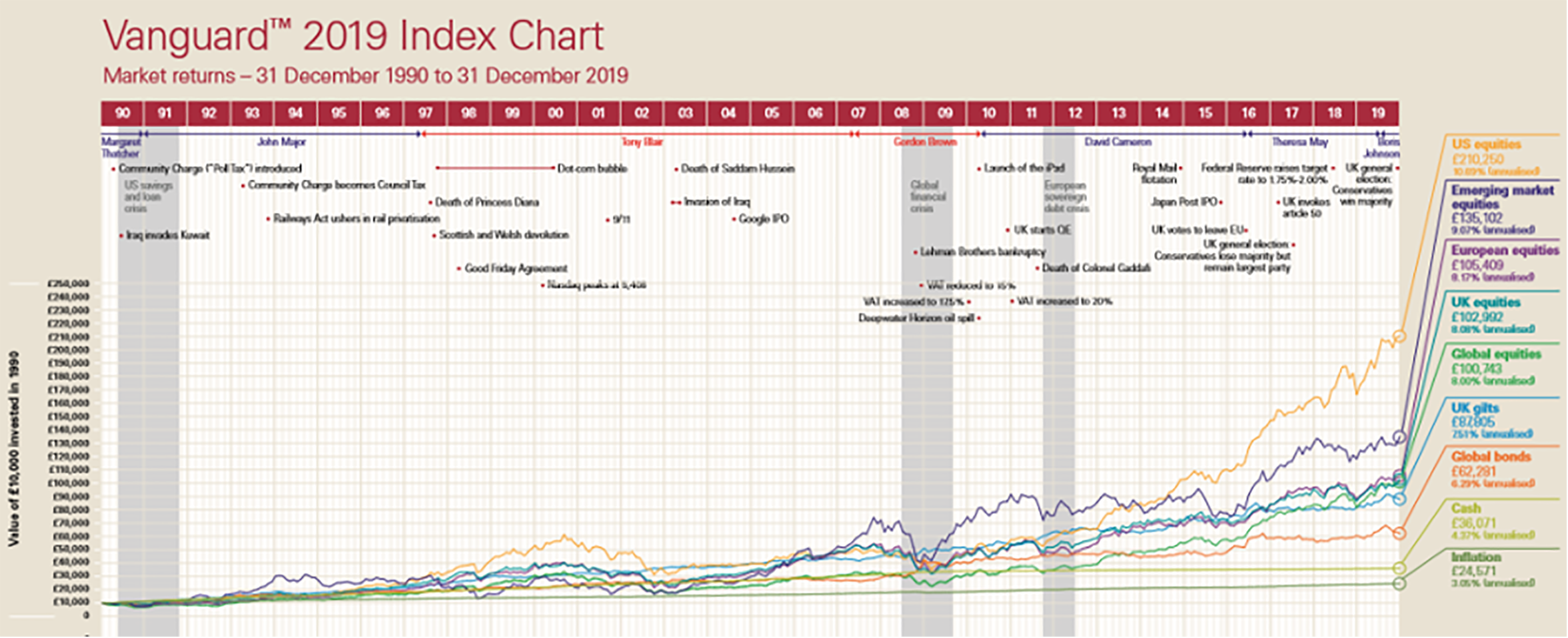

The chart shows the value of £10,000 invested in 1990 in a range of asset classes.

Notes: Cash = ICE LIBOR – GBP 3 month; global equities = the MSCI World Index; US equities = S&P 500; UK equities = FTSE All-Share; inflation = Retail Price Index, (Jan 1987=100); global bonds = Bloomberg Barclays Global Aggregate; European equities = MSCI Europe; UK gilts = ICE BofA; UK gilt (local total return) emerging market equities = MSCI emerging markets; all shown gross of taxes and of fees and in GBP.

Source: Bloomberg and Factset and Bank of England, as at 31 December 2019

Here, you will see that if you’d kept your £10,000 in cash, you’d have generated a return that beat inflation. Your savings would have grown to £36,071.

However, if you’d invested your £10,000 in UK equities in 1990, it would have been worth almost three times as much (£102,992) in 2019. If you’d invested in US equities, you’d have generated a return more than five times better, with your £10,000 growing to £210,250.

Imagine what a retirement that would have bought you, compared to being cautious and leaving your money in cash!

Working with a financial planner can ensure you get the balance right

Every investor is different, which is why it’s so important to have a bespoke plan that fits your circumstances. You might have different sources of income, different life goals, and a different tax situation from other clients.

What we can do is put a robust plan in place to ensure you can life the lifestyle you want with the money you have. If you don’t, you could end up being too cautious in later years and risk running out of money.

An initial chat is always at our expense, so please get in touch to find out more about how we can help you manage your income in retirement. Contact us today or call 01372 404417.

Please note

The value of your investment (and any income from them) can go down as well as up and you may not get back the full amount you invested. Past performance is not a reliable indicator of future performance. Investments should be considered over the longer term and should fit in with your overall attitude to risk and financial circumstances.

A pension is a long-term investment not normally accessible until 55 (57 from April 2028). The value of your investment (and any income from them) can go down as well as up which would have an impact on the level of pension benefits available.

Your pension income could also be affected by the interest rates at the time you take your benefits. The tax implications of pension withdrawals will be based on your individual circumstances. Levels, bases of and reliefs from taxation may change in subsequent Finance Acts.