Back in 2018, insurer Sun Life asked the over-50s what they most wanted to do with their retirement. It won’t surprise you to discover that travel played a large part, with riding a gondola in Venice, experiencing the Northern Lights, and seeing a volcano towards the top of the list.

Other bucket list items including taking a helicopter ride and learning a new language.

Whatever your plans for your post-work years, you’ve spent your working life saving hard to create the lifestyle you want. You have probably been putting money aside every month for years in order to provide a nest egg for your future.

But rather than sit back in your garden with a gin and tonic, retirement can sometimes be the most stressful time of all – without the right planning.

The pension pot you’ve conscientiously saved now has to last you 20, 30 or even 40 years. Even if you’re comfortably off, you then face the prospect of dying with too much and the taxman taking 40% of your wealth.

There are other risks that may hinder your aim to live the lifestyle you want in retirement. Here are three of the most serious, and a solution that can help you mitigate all these risks (and more).

- Sequence risk

The most significant risk to maintaining a lifetime income from your portfolio is known as “sequence risk”.

When you retire, returns in the early period of your retirement have a disproportionate effect on the overall outcome, regardless of the long-term returns over the entire period of your retirement.

Sequence risk is simply the risk that the “order” of investment returns is going to be unfavourable.

Research shows that your investment return in the first ten years of retirement largely determines whether you’re likely to run out of money over a typical 30-year period.

If you get good returns in the early part of retirement, you’re unlikely to run out of money. If you get poor or even mediocre returns in the early part of retirement, you run the risk of draining your pension fund.

Sequence risk is the number one investment risk to manage in your retirement, as the risk will be exacerbated by withdrawals from a portfolio.

- Inflation

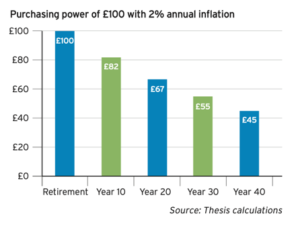

If you live for 20 years after you retire, the simple fact is that £100 withdrawn from your fund now will be worth less in real terms in two decade’s time.

So, over time, either your spending power will decrease, or you’ll have to increase the amount of income you are drawing to stand still.

Source: Thesis

Even if inflation is in line with the Bank of England’s target of 2% per annum, your spending power has reduced by a third in 20 years, and by more than half after 40 years. Of course, if inflation is higher than this then the impact will be more significant.

The 70s were particularly painful, when inflation was in double digits for approximately half the decade and peaked at 22.6% in 1975.

The risk partly depends on your spending plans during retirement. If you intend to spend a lot in the early years as you’re healthy and well, and relatively littler later on, then inflation might not be as big a risk.

However, if you intend to draw a steady income throughout your entire retirement, you have to consider the value of your pot will be eroded in real terms by inflation.

- Not spending carefully

If you head into retirement, start drawing 8% of the value of your pension fund each year, and spend the cash on lavish holidays and luxuries, there’s a strong chance you’ll run out of money.

Indeed, taking any more than around 4% of the value of your fund each year could see you run out of money in later life. Read more about this in our blog about sustainable withdrawals.

Conversely, if you retire, turn down the central heating and spend your holidays in the garden, there’s a strong chance you’ll end up with too much money when you die. Then, all that will happen is that the taxman will potentially take 40% of your wealth as Inheritance Tax.

Not only that but imagine being aged eighty-five and looking back on life and regretting not doing more when you could.

As a financial planner, there is no better feeling than telling clients to go out and spend their money.

I’m not talking about taking a suitcase of used ten-dollar bills to Las Vegas. I’m talking about showing clients that withdrawals are sustainable, modelling risks such as market volatility, and demonstrating in black and white that yes, they can afford to spend and not run out of money – even if they live to 100.

We have some clever software that helps us, and boy does it make a difference to our client’s lives. Hear Rosie’s experience of our “lifestyle improvement process”.

There is one simple way to manage all these risks and more

Managing your income in retirement can be a tricky business. Get it wrong and you could pay too much tax, be unable to meet some of your life goals and, in the worst-case scenario, run out of money.

There is one simple way to manage many of these risks: have a plan.

Research by financial analysts Moneyfacts found that clients who access their pension savings without first taking financial advice are three times more likely to run out of money than people who work with a financial planner.

Moneyfacts head of pensions Richard Eagling says: “The fact that those individuals going it alone with their drawdown strategies are almost three times more likely to have depleted their fund compared with those taking professional advice should be a red flag moment.”

We’ll work closely with you to devise a plan for your retirement, establish sustainable income and spending strategies, and mitigate sequence and inflation risks. While this sounds complicated, the end result is simple: you’ll get to enjoy the lifestyle you want in retirement.

An initial chat is always at our expense, so please get in touch to find out more about how we can help you manage your income in retirement. Contact us today or call 01372 404417.

Please note

The value of your investment (and any income from them) can go down as well as up and you may not get back the full amount you invested. Past performance is not a reliable indicator of future performance. Investments should be considered over the longer term and should fit in with your overall attitude to risk and financial circumstances.

A pension is a long-term investment not normally accessible until 55 (57 from April 2028). The value of your investment (and any income from them) can go down as well as up which would have an impact on the level of pension benefits available.

Your pension income could also be affected by the interest rates at the time you take your benefits. The tax implications of pension withdrawals will be based on your individual circumstances. Levels, bases of and reliefs from taxation may change in subsequent Finance Acts.